This article was originally written on 11th Jan 2024 and later brought to this platform.

NPST was about INR 300 1 year ago and today its at INR 2,409. That is a whopping 8x return in 1 year. No stop. Think. 8x in one year.

The financials are just off the charts: TTM revenue is 84 Crs and the 12 months preceding that was 20 Cr. At the same time PAT has gone from 2 Cr to 16 Cr. Again, 8x in one year.

So yeah… They really have knocked it out of the park. AND even now, they have provided a 15% QOQ top line growth guidance for the next 8 quarters.

What sorcery is this?

NPST has traditionally been a Technology Service Provider (TSP) to Banks. Think Infosys like player who builds tech solutions for the banks. This got them revenue, but it came as a project fee with some aspect of recurring revenue for the AMC they provided.

They built a bunch of products for various banks – the main ones being a payment switch for both the IMPS and UPI payments and more recently a white label super app for banks, merchant onboarding solutions and one stop complaint handling solution. If you don’t understand what these are, that’s okay. All of these are the unsexy part of the story, and we can ignore it (although it is this business that enables their new “sexy” business).

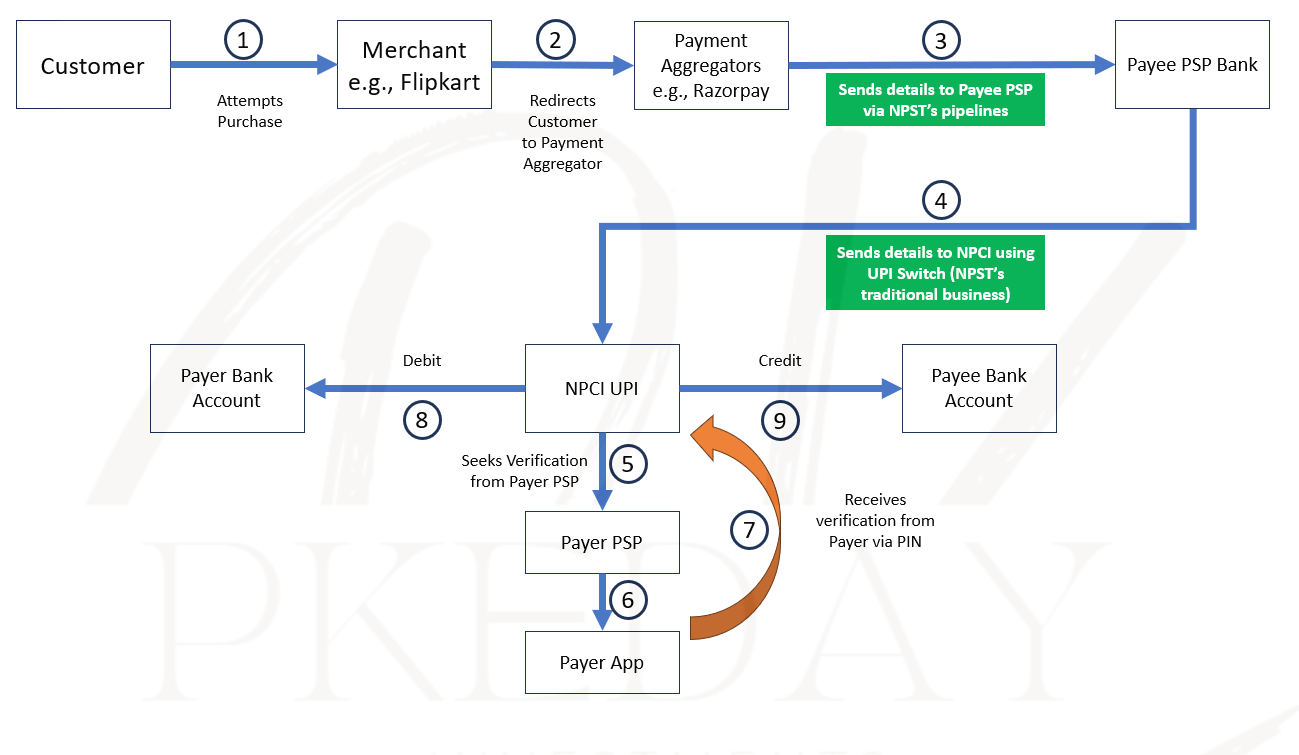

A few years back however, they decided to invest in building a solution for the Payment Aggregators (PAs) rather than the Banks. This solution has enabled them to exponentially increase their revenue as it now linked to Gross Transaction Value.

What is this new solution?

To understand this, you need to first know what a PA (their customer) does.

What are PAs?

These are your Razorpay, PayU, Billdesk – basically the redirects your favourite website sends you to complete the final leg of the transaction (where you put OTP for example).

What do they need from NPST?

RBI has structured the UPI ecosystem (for that matter the whole payment ecosystem) in a manner where the only entities that are allowed to communicate with the NPCI servers (where UPI platform is “running”) are the banks. Thus, whenever a PA needs to process a UPI payment, the PA needs to the help of these banks (a.k.a Payee PSP / Acquirer PSP) to be the messenger on their behalf.

To enable the whole thing, the Payee PSP needs to provide robust and efficient data pipes (a.k.a. APIs) to the PAs which will allow the PA to communicate with NPCI digitally without manual intervention.

Now, banks do not necessarily have the biggest incentive to build these out, at least not as efficiently as desired because technically they aren’t allowed to charge anything for this. Plus, it requires a tech DNA which the banks lacked. So large fintech players like Razorpay have built the entire pipeline for some of these banks which they then use for their (PA’s) captive usage.

These larger players and early movers had the advantage, technological capability and financial muscle to build these APIs for the banks, however, the newer and smaller players (tail end PAs) may not have the same resources.

These are the ones that will be NPST’s customers. NPST offers them a robust set of APIs readily available which makes launching a new PA easy and fast. As of now, as per my knowledge, they remain the only non-banking entity that is providing this solution to 3rd party PAs. Hence, they claim, they are gaining market share among the tail end PAs.

So, what now? Sky is the limit?

Well, that depends on the fate of the tail end PAs themselves. If the tail end PAs survive and even thrive then NPST can grow with them. If the PA industry goes through consolidation (either by the smaller players getting muscled out or bought over) then NPST could be looking at the shrinking TAM.

Consolidation may occur if:

- The large PAs burn cash to capture market share and thus drive the smaller players out of the market with predatory pricing. But one has the wonder why they would do this. Unless there is a larger prize waiting for them at the end of this tunnel, burning money to raise market share seems like a waste of equity. Could they hope to eventually enter the lending space? Maybe.

- The larger PAs start acquiring the smaller PAs. But for this to happen it would imply that the smaller PAs have something to offer and should GAIN market share in the immediate future.

I am not sure how this dynamic will play out and can only say that we need to wait and watch.

That said, it would be unjust for me to link NPST’s fate ONLY with tail end PAs. NPST could sell to the larger PAs as well (just less profitable) and not to mention they could evolve their proposition further: They have already stated their plan to expand their current 5 APIs to 30+ APIs and increase the services for their Fintech partners. The promoters are also happy to admit that they belong to a young and dynamic industry where staying still means going backwards. So they might have some more tricks up their sleeve.

But isn’t it too expensive?

At 98 PE it is among the more expensive stocks out there. But with a 15% QoQ guidance (which they have delivered on for 2Qs so far, this seems like an easy fix:

If we can trust on the guidance, NPST is at a 1 year forward PE of 45-50. If the growth can sustain post 1 year from now, there is no reason to assume the PE will come down.

So, what do we do?

I think investing a small amount in NPST right now is worth the risk. Because even if the industry goes through consolidation, it will take some time and NPST revenues are clearly in momentum for the time being.

If the smaller players are getting bullied or bought out AND NPST fails to expand its TAM by developing more value propositions, then we need to rethink NPSTs long term story. If they are successful in doing so, then NPST can be one of the best value creation opportunities in the market right now.

This is a risky bet though and tracking the industry and how the dynamics are playing out is critical. Unfortunately, I have not found any source to track this – and if any reader has some ideas please do share. If you know some people in these tail end PAs, do connect with them as well. It would be great to hear this from the horse’s mouth.

I have also not managed to connect with any of NPST’s customers to get a testimonial from them. If you know people in these companies, please do connect me as well:

- Easy Pay

- Airpay

- PayFi

- IndussPay

Disclaimer: I hold a stake in NPST. I am not an investment advisor. This is not investment advice.